Doom decides between following his original IPS and going all in on gold goblets.

Today I’m going to talk about Investment Policy Statements. I’m creeping up on my early retirement date, set for April of this year, which has triggered a review process of my own IPS, and I wanted to share the details.

So, first things first. What’s an investment policy statement? It’s a document that a portfolio manager generates which details objectives of the client, along with corresponding rules and guidelines to follow in order to, hopefully, meet those objectives. Objectives are simple life goals, such as: Create an emergency fund to cover 6 months expenses. Accumulate sufficient assets to retire by 55 off passive income. And so on.

Strategies are then created to satisfy the life objectives of the client. These are added to the document along with other structure-providing parameters. An IPS is basically your your investing blueprint.

Now, in the case of self-managed portfolios, like mine, the investment policy statement is something you, the individual investor, create and pledge to follow for yourself. Because, hey, you are your own portfolio manager.

It’s a personal investment manifesto, a document that you will follow through thick and thin, because you’ve done your research, assessed your goals, and come to definite conclusions about how you want to manage your savings in order to meet those objectives.

If you don’t have one, chances are pretty good that you’ll be tempted at some point to change yours, too. You may be influenced by day-to-day events or news headlines. The advice of a well-meaning friend. Or maybe the age-old standbys: Fear and Greed.

In nearly every case, it’s be a bad idea to change your previously-defined strategy. There are only a few so-called qualifying events which may justify a change of course. If you haven’t hit such an event, you’ll almost certainly be best served by sticking to your original plan.

Because when you’re index-investing for the long-haul, the right move is usually making no moves at all.

Simple or Complicated

Investment policy statements can be incredibly simple or staggeringly complex.

Let’s look at a two examples, so you get the feel of what’s on the table here.

Example 1: Simple

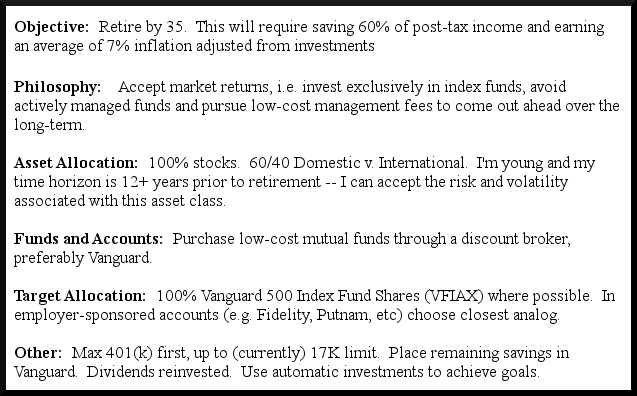

A bare-bones IPS has only a handful of entries.

Philosophy, Asset Allocation, Funds/Accounts, Target Allocation

And there’s nothing wrong with the simple version. In fact, the first IPS I created, back in 2002, had exactly the above fields. It looked like this:

The above is suitable for many people in the accumulation phase of their early-retirement journey.

Example 2: Complex

As people get move through life, it’s common for goals to change. When you create your first IPS, you might be in your early 20s, single, fresh out of school, pulling a good income, relatively footloose.

However, the world might look quite a bit different when you’re 35 or 40. Maybe you’ll have children, a single family residence, aging parents who rely on you, or a change in income streams from employment to taking distributions from your assets.

Your IPS should therefore be updated to reflect the new realities.

Considerations which may be added to the ‘simple’ version include:

- Inheritance-Related Objectives

- Drawdown Strategies

- Details Regarding Mortgage Payoff Plans

- Granular Performance Goals

- Risk Tolerance Profile

- Annual Passive Income Targets

- Tax-Minimization Tactics

- Review Periods

- Rebalancing Criteria and Methodologies

- Other ‘Monitoring’ procedures to help stay on track

Check out the Boglehead wiki for additional ideas on useful items to add to your own IPS. (Bogleheads are pretty insistent on every investor creating their own governing policy statement.)

Updating Your IPS

So I’ve been promising for a while, in other recent blog posts, to talk about the transition between working and early retirement. You therefore might be wondering why I am instead going on and on about finances and Investment Policy Statements and blah blah blah.

The thing is, retirement is a so-called qualifying event which triggers a review of your investment plan. Reviewing the blueprint behind your investment strategy is a critical part of managing the upcoming change.

And there you have it: I’m retiring in a couple of months, so I’m reviewing my IPS.

Other qualifying events might include:

- A new job

- The death of a spouse — or a new one (AKA change in marital status.)

- Additional dependents — perhaps you had some kids or (gasp!) your parents moved in

- A move to another location with a different COL, perhaps another country

- Significant changes to the health status of yourself or a family member

- Hitting other retirement age milestones. For example:

- 59 1/2 for penalty-free withdrawals from tax advantaged accounts, e.g. 401(k), 403(b), IRAs

- 62 for minimum social security eligibility (Got to keep an eye on this age. It may change.)

- Pension Eligibility ages

You get the idea. If you haven’t hit a qualifying event, it’s best to stay the course: Simply continue executing your current plan.

And please note that there is no mention of using market movements of any sort as a qualifying event. For example, bonds dropping by 20% is not a valid reason to update your policy statement to change your asset allocation or overall strategy.

The market event should instead trigger a rebalance during your annual review so you can get back to the asset allocation specified in your policy statement.

Personal Review

First off: I’ve been using a 70/20/10 stock/bond/REIT split on my asset allocation since 2008. The one-sentence justification for this, as stated on my IPS, is: Stocks will drive growth, bonds will reduce volatility, and REITs (which loosely track ETF indexes) should diversify a tad more as they are tied to “real world” assets. They also produce decent dividends.

Other than the difference in asset allocation, my 2008 IPS is almost identical to the 2002 version in the image above, in “Example 1.”

Fast forward to today, and the only change I’m making as a result of the current review is to exchange my 10% REIT allocation directly to bonds.

The justification for this change is that the accumulation phase of my life is over. My projected draw off of assets is 2.6%. I can therefore move toward a slightly less volatile asset allocation, which, in turn, has generated lower historical returns. Like I mentioned above, REITs loosely track stocks (and are historically more volatile than bonds) so going to a straight 70/30 split should both simplify and stabilize my portfolio a bit.

It’s also the same allocation as one of my heroes, Mr. Collins in New Hampshire, so I’ll be in good company with this plan.

Although some respected Boglehead-ish investors (such as Rick Ferri, who suggests an opposite split, 30/70) advocate a higher ratio of bonds in retirement, I will personally not go below 70% in US Equities for the following reasons:

- Historically, bonds have produced negative real returns for longer intervals than stocks. Holding too much of your allocation in bonds is actually quite risky, especially for a super early retiree, like someone under 45. Compared to your average retiree, you’re going to need an extra two decades of living expenses, and you’ll need market growth to generate it for you.

- During 1802–2001, the worst 1-year returns for stocks and bonds were -38.6% and -21.9% respectively. However for a holding period of 10-years, the worst performance for stocks and bonds were -4.1% and -5.4%; and for a holding period of 15+ years, stocks have always been profitable, whereas bonds have undergone a negative 20-year period (1946-1966, -1.2%) as well as a 15-year patch of malaise (1966-1981, -4.2%).

- Stocks are a better hedge against inflation than bonds, which historically have gotten destroyed during inflationary periods. Now I’m no inflation hawk, but still, I want to be covered against multiple scenarios of our mutually unknowable future.

- Take a look at the Trinity Studies. There are charts examining the success rates of various asset allocation mixes throughout history. The data clearly shows better success rates with higher allocations of stock, i.e. a 75/25 stock/bond split has a greater chance of producing long-term success than a 50/50 split. This chart illustrates the power of holding ETFs even as it fingers an overweight allocation of bonds as a risk.

Bottom line: I will be transferring my current 10% REIT holding into Vanguard Total Bond (VBTLX) as a 1-time move. Since I hold REIT in a tax-advantaged account, I can make this exchange without any tax implications.

3. During this review I added a new section to my IPS: “Triggers” to review finances.

- Checkpoint Mid-July, triggered by Google Calendar reminder

- Checkpoint Mid-December, same trigger. Evaluate any changes to tax code that might require plan updates.

- Checkpoint in Mid-Jan, when I pull out my annual COL 20K — I’ll be in the drawdown phase starting next year.

4. Also a new section “Misc” which includes a few things

- An explicit goal to not check account holdings at any times other than review periods listed above. Most people benefit from not frequently checking balances. If you are an index investor, it’s not helpful to engage in compulsive account micro-management, and in fact, this activity can lead to impulsive decision-making. I plan to think about finances as little as possible in retirement and not checking balances is part of this objective.

- Some additional actionable items from my drawdown strategy.

- I updated my rebalancing strategy to the following: This activity will take place once a year, also in mid-Jan. In my tax-advantaged accounts, I will do this every year, regardless of percentage. In the taxable accounts, I will follow gain and loss harvesting strategies to reduce my taxable burden while simultaneously working back toward my 70/30 split.

This will probably be the last financially-driven blog post for a while, as I can’t see any further need to rake over the finances until the checkpoints detailed in my plan.

Nice to have that all sorted out.

Takeaways

Creating and maintaining a personal investment policy statement is an important step for individual investors. It is your strategical cornerstone, a document of your beliefs and objectives that you will return to in times of uncertainty. If you can’t explain your investing strategy in an IPS, you may not be ready to invest yet. Instead, you should read books and blogs on the subject until you’ve formulated opinions that you’re comfortable sticking with, through good times and bad.

And about those bad times. I remember investing through the extended crash between 2008 and 2010, when it seemed like everyone around me was moving into less conventional stuff: Gold and silver, focusing on ‘commodity stocks’ or exchange-rate based trading, even hiding cash under mattresses in case the banks failed utterly. To index investors, these knee-jerk reactions are pretty stupid, but based on how these assets were doing in the short term, they looked pretty good. People at work bragged about suddenly getting ‘awesome’ returns now that they were ‘out of the general market’ and into ‘sectors.’

During this time I literally printed out a copy of my IPS, put it in my desk drawer, and read it when doubts started creeping in. At one point, in the beginning of 2009 when the S&P 500 was down to 800 or so, going over my policy statement prompted me to actually re-read the entirety of John Bogle’s Common Sense on Mutual Funds to see if it still made sense to be an index investor. (Bogle is the founder of Vanguard and is viewed as the father of index investing.)

Answer: Of course it did. Reviewing the material helped re-affirm the logic of index investing and therefore fortified my position even during those times of immense losses.

Because sticking to your plan is the best way to achieve the results you want.

As a final point, let me share a 10-year snapshot of earnings from my Vanguard account.

The green section represents only investment returns from my Vanguard account. It does not include account balances.

Look, the majority of people change their asset allocation and investment profile when things get tough. I’m not guessing here — the difference between market returns and investor returns (a very significant 40%+ drop) is called the behavior gap, and it’s caused by people making emotional moves with their money. We’re human beings, after all — not robots. We want to take action to fight adversity, dammit, action!

But in this case, action is the worst possible thing for your portfolio. You’ll need every resource available to help you instead stay the course, enabling you to eventually earn the market returns your retirement plans depend on.

Including, and perhaps especially, an IPS.

Additional Resources

- IPS template from Morningstar and corresponding article

- IPS information and sample from the Bogleheads wiki

{kind=link}

The hardest part of your IPS I think would be to “not check account holdings at any times other than review periods listed above.” I check mine at least daily… Why? I don’t know really. I think it stems from the fact that I like to make sure nothing has happened to my hard earned money! But this is definitely a habit I’m trying to reduce!

Only 2 months left livingafi!!!

Hey FF

I think it’s OK to go through parts of your accumulation phase checking balances a fair amount. Watching the swings gives you a feeling about how the market works on your assets that can’t quite be taught.

That being said, checking every day isn’t not going to make your assets grow any faster — or shrink any less when things are going down. I want to avoid becoming one of those people that obsesses on the money after I stop working. Some people most definitely do, though my opinion is that if you’re thinking about your account balances every day after pulling the plug on employment, you’re not doing FIRE right.

2 freaking months. Incredible.

Agreed, I think the more I “mature” as I go down this FIRE journey, the less I’ll be inclined to check the balances daily. And the market swings don’t really bother me as I know what my end goal is, so I really don’t know why I do it!

Thanks for posting this, you gave me the motivation I needed to finish the draft of my own IPS that had been hanging around 90% complete. I’ve posted it over at the MMM forums if you have time to check it out. Here is the link: http://forum.mrmoneymustache.com/investor-alley/australian-case-studyinvestment-policy-statement-review/

Cheers,

Shaz

Shaz: It’s solid for the most part. If you’re in the very early phases of accumulation, you might want to be closer to 100% in stock, shifting the ratio a bit as your assets begin to pile up and you have more to lose. Definitely wouldn’t go lower than 80/20 during this period, but many (most?) people on this path are higher in stocks.

Another point: Your goal is to hit FI in 17 years. The math behind early retirement shows that you’ll need 50% savings rate plus 5% “real” (inflation adjusted) returns over that duration. Does your investment strategy support these requirements?

I’m not qualified to comment on the AU-specific parts of your plan so I can’t crunch these numbers for you, but that’s where I’d focus my energy. Looks like a few other people on that thread added some thoughtful guidance as well, particularly bigchrisb’s ideas about looking at your AA ‘in aggregate’ — across accounts.

You’re close!

Thanks for the post and timely reminder for me to finally pen a formal IPS, instead of relying on assorted notes and comments in my spreadsheet !

Just one comment/correction re: “Rick Ferri, recommends a 60/40 stock/bond split for retirees, calling it the ‘center of gravity.’ ” Please re-check on this point, as I think his recent blog proposes a 30/70 center of gravity for retirees (versus 60/40 for accumulators). I recall this from a recent MMM thread on it where several people were questioning his stance as being too conservative, here it is : http://forum.mrmoneymustache.com/investor-alley/rick-ferri-3070-portfolio-for-retirees/msg546641/#msg546641

I like your final point a very clear illustration of the importance of staying the course.

FFA, thanks for the prompt to re-check the Ferri source. You’re right. He’s suggesting 60/40 as a starting point for accumulation and 30/70 for retirees. I do think this is too conservative, especially for very early retirees, who, as I mentioned, will need more growth over the long-haul to power their portfolios through an extra couple of decades. I’ll update the post, don’t want to misrepresent Ferri’s views. And for the record I wouldn’t be lower than than 80% stock for the accumulation phase. You can make a strong case for being all in at 100% for this period, only switching your AA once you’re fairly close to hitting your ER milestone. (Hell, some people are planning on staying 100% stock in retirement. You can make a logical case for that, too, but my risk tolerance is lower.)

I just read the MMM thread too, thanks for that. The FireCalc sims clearly make the point I was angling toward. If you have a lot of years ahead of you, a 30/70 split isn’t going to result in much success.

Happy IPS’ing!

Yup we’re basically on the same page. I think especially in the world of early retirement it’s appropriate to be holding much higher stock allocations. I believe the context of Ferri’s article is conventional retirement, which even still involves increasing longevity these days.

Sorry it’s getting more into AA but since we’re touching on it… One concern I often have reading FIRE forums and especially when it gets into Firecalc sims, etc : It seems to me that many people approach the problem backwards. i.e. I need a to take an 80/20 allocation in order to meet my target retirement date. (Input : end date // Output : required AA)

Instead, the safer/better approach in my mind: Develop a proper self awareness of personal risk tolerance, adopt a compatible AA which can be held comfortably for long term and ride the swings. Then based on this forecast a retirement date. (Input : risk tolerance -> AA // Output : end date).

If the end date is later than desired, first make adjustments to controllable factors (e.g. spending) to bring closer to target. Choosing a higher AA is an easy choice, and it might be appropriate too but really should be underpinned (e.g. financial self-education, take financial advice if needed, put together a solid IPS and follow it, etc). These actions can conceivably make a tangible improvement to the person’s risk tolerance and justify the assumption of a higher AA. Otherwise, it feels to me like a shortcut to a faster retirement on paper, but who knows what will happen in the real world and if this AA can be sustained….

Anyway, enough procrastination by me, I think I’ll fire up Word and get on with this much belated task myself of IPS’ing 🙂

I have similar thoughts and completely agree that judging your own risk tolerance is crucial. It’s why I maintained a 70/20/10 split even during accumulation, even though “100% stock” in theory gets you to FIRE faster. I appreciate the drop in volatility and recognized that the more conservative allocation was worth potentially extending my working life by perhaps half a year to a year — a good trade for me. This is all an inexact science anyway, since we’re predicting the future using past data, there’s no guarantee that the future will be like the past. It’s rational to believe that it is likely to be similar, but not rational to think there’s no risk.

>> first make adjustments to controllable factors (e.g. spending) to bring closer to target.

Spot on. For people starting out — (< 5 years into FIRE) your savings rate is so much more important than your AA it's not even close. It's only once you're in the middle that your investment choices start to matter. By the end, though, it's crucial that you pick something that will safely fund you as you take distributions. The problem with judging your own risk tolerance is that you don't really know what it is until you've lived through some turbulent times. (Also, lots of folks are bad at evaluating and predicting their own behavior.) For many people in the early phases, all they've seen is the market runup of the past 5-6 years, making it easy to say "Yeah, 100% stocks."

Speaking of procrastination, it's time for me to get my run in before another blissful day in the office starts up. 🙂

” 70% in US Equities”

I would not be so much in US Equities alone, but put in a international component.

Pingback: Publishing my Investment Policy Statement | FIRE v London

That chart is amazing. Well done.